What You Need To Know

Buying a business is exciting, confusing, intimidating, and occasionally makes you question your life choices. Totally normal.

At VI Business Brokers, we guide buyers through a structured process built on real-world acquisitions and not theory. This updated 10-step framework is based on our internal process and the principles outlined in our Buy Then Grow book.

Think of this as your roadmap. Or your GPS. Or that friend who already made the expensive mistakes so you don’t have to.

Step 1 – Where to Begin (Mindset + Self-Awareness)

Before you look at listings or run numbers, you need to take a step back and look at yourself.

Most first-time buyers focus on what business to buy, but experienced buyers start with a different question: what kind of owner do I want to be? The answer shapes everything that follows. Some people want to operate a business full-time, while others prefer to own something more passive. Some want growth and scale, while others want stability and cash flow.

You also need to be honest about your strengths. If you are strong in sales, you may thrive in a service business. If you are operationally focused, something process-driven may suit you better. The biggest mistake buyers make early is chasing businesses that look exciting instead of ones that actually fit their skill set.

Owning a business is not passive. You will be thinking about it constantly, especially in the beginning. That is why alignment matters so much. You are not buying a fantasy. You are buying a real operation with real people, real problems, and real responsibilities.

When this step is done properly, everything else becomes easier. When it is skipped, everything becomes harder.

Step 2 – How Much Do You Really Need to Buy

One of the biggest misconceptions in business buying is how much capital is required. Many buyers assume they need to pay for the entire business in cash. In reality, very few deals are structured that way.

Banks do not lend based on ideas but they lend on cash flow. If a business consistently generates profit, lenders are far more willing to finance a large portion of the purchase. On top of that, sellers are often willing to finance part of the deal themselves, especially if it helps bridge the gap and get the deal closed.

A typical acquisition might be structured with:

- A majority bank loan

- A portion of seller financing

- A smaller cash contribution from the buyer

This means buyers can often acquire businesses with far less capital than expected.

Before even getting to this stage, many buyers go through a prequalification process to confirm they are financially ready and taken seriously by lenders and sellers. If you want to understand what that looks like, you can read more about buyer prequalification and proof of funds.

The real question is not whether you can afford the purchase price. The real question is whether the business can comfortably support the debt after you take over. Strong cash flow solves most financing problems. Weak cash flow creates them.

Step 3 – Finding Deals That Actually Close

Finding a business is not the challenge. Finding a good business that actually closes is.

The reality is that most deals never happen. A large percentage of listed businesses sit on the market for months or years without selling. This is usually due to unrealistic pricing, poor financials, or sellers who are not truly motivated.

Successful buyers treat deal sourcing as a process, not a one-time event. They review many opportunities, filter aggressively, and focus their energy on situations where a transaction is actually possible.

Deals typically come from a few key sources:

- Business brokers and marketplaces

- Personal and professional networks

- Direct outreach to owners

- Strategic positioning online

However, the highest-quality deals are often off-market, where there is less competition and more flexibility in structuring.

A simple mindset shift helps here: do not chase listings but identify motivated sellers. Motivation is often the difference between a deal that drags on and one that actually closes.

Step 4 – Is This a Growing or Dying Industry

Even the best operator will struggle in the wrong industry. This is why industry selection is one of the most underrated parts of the buying process.

It is easy to get distracted by trends or “exciting” sectors, but attention does not equal durability. Many fast-growing industries disappear just as quickly as they appear. On the other hand, some of the most stable and profitable businesses operate in industries that most people would consider boring.

The key is to focus on businesses that solve recurring, necessary problems. Industries tied to essential services tend to perform consistently, regardless of economic cycles or trends.

When evaluating an industry, it helps to ask:

- Is demand consistent over time?

- Is the service or product necessary?

- Can it be easily replaced or disrupted?

In many cases, the safest opportunities are not the most exciting ones. They are the ones that quietly generate cash flow year after year.

Step 5 – Understanding Financials (Without Being an Accountant)

You do not need to be an accountant to buy a business, but you do need to understand how the business makes money.

Financial statements are not just documents and they are the story of how the business operates. They show whether revenue is growing or shrinking, whether costs are under control, and whether the business is actually generating usable cash.

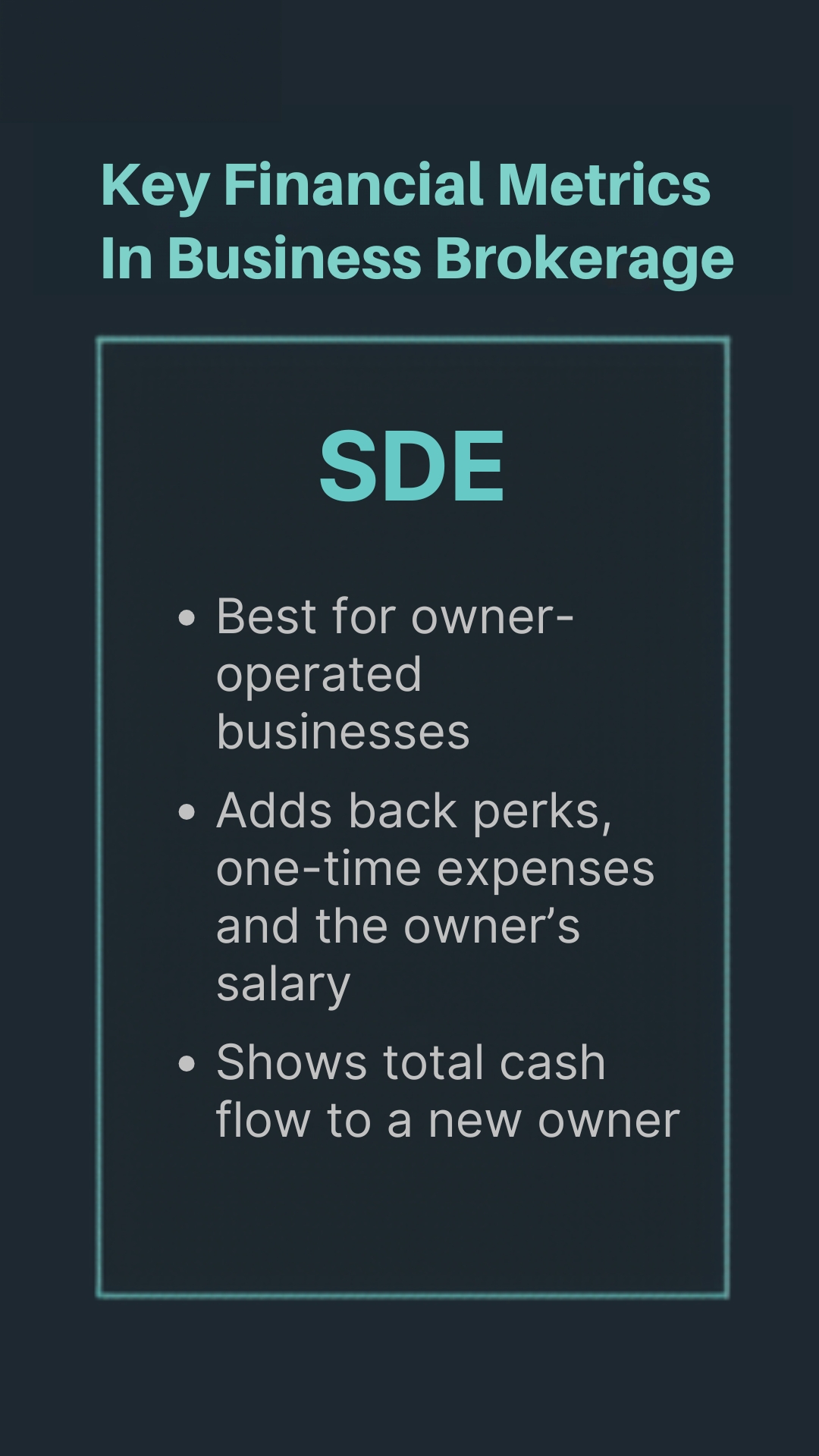

For small businesses, the most important metric is Seller’s Discretionary Earnings (SDE). This represents the total financial benefit available to an owner-operator and gives you the clearest picture of what the business can realistically produce for you.

At this stage, it is also important to approach financials with a balanced mindset. Sellers are not usually trying to mislead buyers, but their numbers often reflect years of habits, assumptions, and informal bookkeeping. This is why verification matters.

Instead of asking whether the numbers are right or wrong, the better question is: are these numbers reliable and repeatable under new ownership?

Step 6 – What a Business Is Actually Worth

Valuation is where many buyers either overcomplicate things or oversimplify them.

Most small businesses are valued based on a multiple of their cash flow, typically using SDE. While there are general ranges, there is no single “correct” number. Value depends on a combination of stability, growth potential, risk, and how dependent the business is on the current owner.

It is important to understand that valuation is always a range. Two buyers may look at the same business and come to different conclusions based on their experience, goals, and ability to improve the operation.

If you want a deeper breakdown of how multiples actually work and what buyers are paying in today’s market, you can read our full guide on what is your average business valuation.

Lenders also play a role in valuation, whether buyers realize it or not. If a deal cannot support its debt comfortably, financing becomes difficult, which effectively sets a ceiling on price.

The goal is not to get the lowest price possible. The goal is to pay a price that makes sense for the business you are acquiring and the future you plan to build.

Step 7 – Deal Structure Is More Important Than Price

This is one of the most important concepts in business buying, and one that many first-time buyers overlook.

Price is visible. Structure is what determines whether the deal actually works.

A well-structured deal can:

- Reduce upfront capital requirements

- Protect the buyer from downside risk

- Keep the seller engaged after closing

Tools like seller financing, earn-outs, and working capital adjustments allow buyers to share risk and create alignment between both parties.

In many cases, a slightly higher purchase price with strong terms is far safer than a lower price with poor structure. Smart buyers focus less on the headline number and more on how the deal is built.

Step 8 – Financing the Deal

Once a deal is structured, financing becomes the next step. This is not just a technical process but a presentation.

You are effectively pitching the deal to a lender. They want to understand:

- Who you are

- Why this business makes sense

- How the loan will be repaid

Strong buyers approach financing with preparation. They present clear financials, realistic projections, and a simple, compelling story about the opportunity.

A big part of getting approved is being seen as a “bankable” buyer. This includes your credit profile, experience, and how well you present the deal. If you want to improve your chances with lenders, we break that down HERE.

Lenders evaluate risk using several factors, including your experience, the business’s cash flow, and the overall stability of the industry. When these elements align, financing becomes much easier.

It is also important to manage expectations. Financing takes time, and rushing the process often creates unnecessary stress or risk.

Step 9 – Due Diligence That Actually Matters

Due diligence is where assumptions are tested and verified.

At this stage, you are no longer evaluating the business at a high level. You are confirming that everything you were told is accurate. This includes reviewing financial records, contracts, operations, and any potential risks.

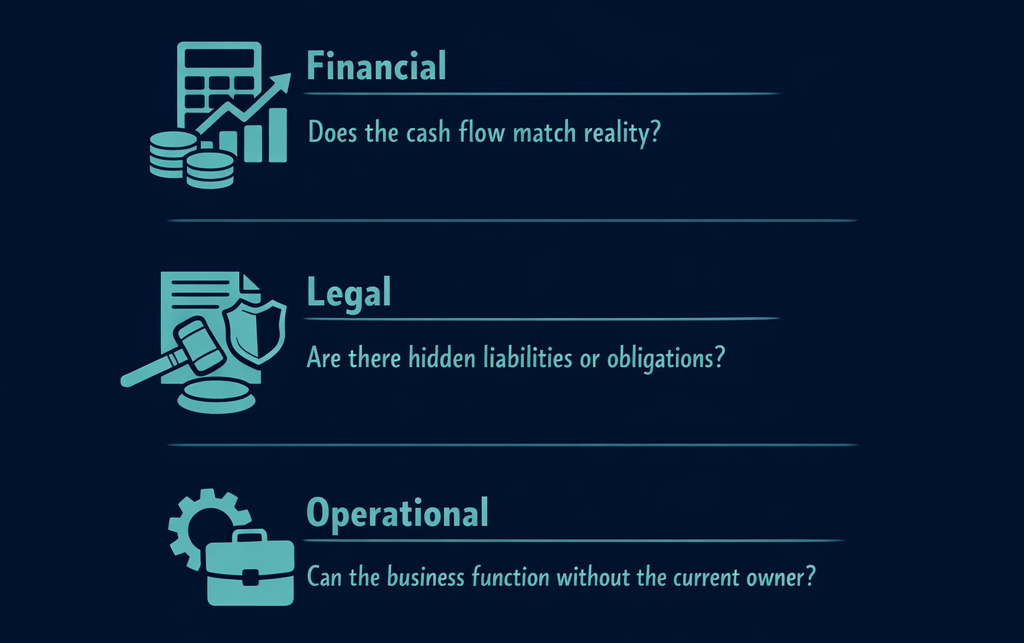

There are three core areas to focus on:

- Financial: Does the cash flow match reality?

- Legal: Are there hidden liabilities or obligations?

- Operational: Can the business function without the current owner?

Many deals fall apart during this phase, not because problems exist, but because they are discovered too late or not communicated clearly. Staying organized, asking the right questions, and maintaining momentum are key to getting through this stage successfully.

Step 10 – Buy Then Grow

Closing the deal is not the finish line. It is the starting point.

The first phase of ownership is about stability. New owners often feel the urge to make immediate changes, but this can create unnecessary disruption. The business was working before you arrived, and your first job is to understand why.

Over time, growth comes from small, consistent improvements. This can include refining pricing, improving marketing, or making operations more efficient. In some cases, growth may also come from acquiring complementary businesses and combining them strategically.

The key is patience. Sustainable growth rarely comes from drastic changes. It comes from disciplined execution over time.

Final Thoughts

Buying a business is not just about replacing income. It is about creating opportunity.

One well-run business can provide stability and cash flow. Multiple businesses, managed strategically, can create long-term wealth and flexibility. This is where the real potential lies.

The buyers who succeed long-term are not the ones chasing quick wins. They are the ones who think in terms of years, not months. They build systems, make thoughtful decisions, and continue to improve over time.

Buying a business does not have to be complicated or overwhelming. When you understand the process and approach it step by step, it becomes far more manageable.

At VI Business Brokers, we guide buyers through every stage with clarity, structure, and real-world experience. Our goal is not just to help you buy a business, but to help you buy the right business and set it up for long-term success.

Because business buying is serious.

But it does not have to be miserable.