If you want to buy a business in Canada using financing, your first job is not finding the business. Your first job is becoming bankable.

Being bankable means a lender looks at you and the deal and says yes, this person can repay the loan without stress. It is about reducing risk in the eyes of the bank. The good news is you do not need to be rich to be bankable. You just need to understand what lenders are looking for and prepare properly.

Most buyers focus on price and negotiations. Banks focus on cash flow, structure, and the borrower. If you understand their lens, you dramatically increase your chances of getting approved.

Commercial Lending Is Different From Buying a House

One important thing many first-time buyers do not realize is that commercial lending is very different from residential mortgages.

When someone stops paying a home mortgage, the bank can typically take the house, sell it, and recover most of the loan.

Businesses are very different.

If a borrower stops making payments on a business loan, there may be very little left for the bank to recover. Equipment can depreciate quickly, goodwill disappears, and sometimes there is nothing meaningful to sell at all.

Because of that risk, lenders are far more conservative when financing business acquisitions.

This is why becoming “bankable” matters so much. The bank is not just evaluating the business. They are evaluating the cash flow, the deal structure, and the buyer behind it.

Fortunately, once you understand what lenders care about, preparing for financing becomes much easier.

Here is what makes you bankable in Canada.

Cash Flow Is King

The number one thing lenders care about is cash flow. Not revenue. Not potential. Not your excitement. Cash flow.

Consistent and predictable cash flow is what makes lenders comfortable. This is one of the reasons startups are much harder to finance. Without a history of stable earnings, the bank has very little data to rely on.

An established business with steady profits, recurring customers, and predictable expenses is far easier to finance because lenders can clearly see how the loan will be repaid.

In other words, banks are not investing in potential. They are investing in proven financial performance.

They want to see that the business generates enough money to cover operating expenses, pay you a reasonable salary, and still have room to make loan payments.

This is where DSCR comes in. Debt Service Coverage Ratio measures whether the business can comfortably handle the debt. Most Canadian lenders want to see a DSCR of at least 1.25. That means the business produces 25 percent more cash than the annual loan payments.

If a business cannot support the debt on paper, it is not financeable no matter how good the story sounds.

This is why a proper cash flow analysis and normalization of financials is critical before going to the bank.

For guidance on how lenders evaluate cash flow, you can review resources from the BDC.

Repayment Capacity Matters More Than Profit

A business can be profitable and still not be financeable.

Banks are not just looking at net income. They are looking at how much real cash is available after adjustments. They want to see that loan payments fit comfortably into the business without choking operations.

If every dollar is already allocated to payroll, rent, and inventory, there is no room for debt even if the income statement shows a profit.

Strong repayment capacity means there is a cushion. It shows the lender that if sales dip for a few months, the business can still survive and pay the loan.

This is especially important for acquisition financing because lenders are evaluating future performance, not just historical numbers.

A simple way to think about repayment capacity is this: after paying all operating expenses and the new loan payment, is there still money left?

If the answer is yes, the deal may work.

If the answer is no, the financing usually stops right there.

Lenders want to see breathing room in the numbers. A business that barely covers its loan payments is considered risky, while a business with healthy leftover cash provides the cushion lenders are looking for.

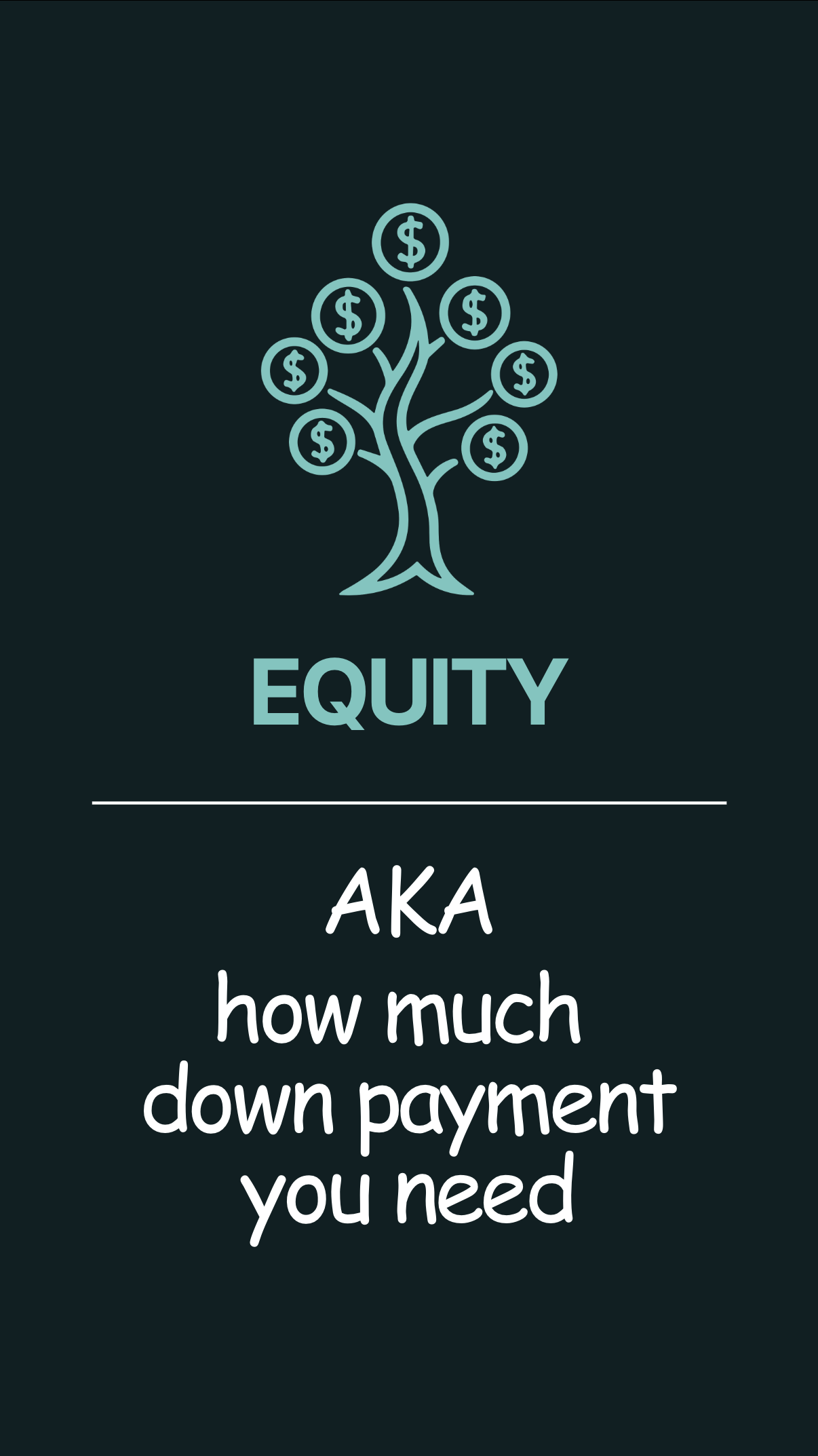

Equity Shows Commitment

In Canada, most acquisition loans require a buyer to put in equity. Typically this is around 10 percent of the purchase price when using programs like the Canada Small Business Financing Program.

Equity does not always have to be cash sitting in a bank account. It can include retained earnings in the business, equipment, or sometimes seller financing that is structured properly.

From the lender’s perspective, equity means you have skin in the game. If you are investing your own money, you are less likely to walk away when things get tough.

You can learn more about equity requirements through the ISED

For a strong, profitable business, buyers should typically expect to contribute around 20 percent of the purchase price as a down payment.

If the business is weaker, riskier, or has inconsistent financials, lenders may require a larger equity contribution.

From the bank’s perspective, equity proves the buyer is committed and financially invested in the outcome.

Management Experience Reduces Risk

You do not need to have owned a business before to be bankable. But you do need to show that you can run this specific business.

If you are buying an HVAC company, lenders want to see operational, technical, or management experience in that field. If you do not have it, you need to show strong advisors, a transition plan with the seller, or a qualified general manager.

Experience reduces execution risk. It answers the question every lender asks which is can this person actually run the business they are buying.

A clear transition plan with the seller staying on for training is one of the easiest ways to strengthen this part of your file.

Your Credit Story Matters

Credit score is important, but it is not the whole story.

Lenders look at your history of managing debt. Do you pay on time. Do you carry high balances. Have you had collections or missed payments.

If there are issues in your credit history, they need to be explained. A strong written credit story that shows improvement and current stability can make a big difference.

Canadian lenders often pull both personal and business credit reports.

Clean credit tells the lender you are financially responsible. It builds confidence that you will treat the loan the same way.

Documentation Wins Deals

One of the biggest reasons deals get delayed or declined is incomplete documentation.

Banks want clean, organized, and professional paperwork. This typically includes three years of financial statements, three years of tax returns, interim financials, bank statements, a business plan, projections, and a detailed use of funds.

Commercial lending requires significantly more documentation than most buyers expect.

Lenders typically want to review:

• Financial statements

• Tax returns

• Cash flow forecasts

• A business plan

• Lease agreements

• Purchase agreements

Being prepared with organized documents not only speeds up the approval process but also signals professionalism and credibility to the lender reviewing the file.

Sloppy documents create doubt. Clean documents create trust.

Your projections should be realistic and tied to the historical performance of the business. Lenders are very good at spotting overly optimistic forecasts.

If your package is complete and well presented, you immediately stand out from most buyers.

The Deal Structure Matters

You can be a strong borrower and still get declined if the deal is structured poorly.

Lenders prefer reasonable purchase prices, strong seller notes, and working capital included in the financing request. They want to see that the business will not be undercapitalized on day one.

Seller financing is one of the most powerful tools for becoming bankable. It shows the seller believes in the business and shares the risk with the lender.

A well structured deal can turn a marginal file into an approved one.

Relationships With the Right Lenders

Not all banks understand acquisition financing.

Many traditional branch lenders are more comfortable with real estate loans than cash flow based business acquisitions. Working with lenders who regularly finance business purchases dramatically improves your odds.

In Canada, institutions like the Royal Bank of Canada and Scotiabank have teams that specialize in business acquisitions.

Community based lenders and economic development organizations can also be valuable partners for first time buyers.

The right lender understands the model and evaluates your deal properly.

Do Not Forget the Hidden Costs of Buying a Business

Another important part of becoming bankable is understanding that the down payment is only one part of the equation.

Business acquisitions also involve several additional costs, including:

- Legal fees

- Accounting reviews

- Loan origination fees

- Appraisals or business valuations

Buyers who fail to budget for these costs can run into financing problems late in the process.

Planning for these expenses ahead of time ensures the transaction stays on track and shows lenders that you have thought through the full financial picture.

Build Your Bankable Profile Before You Make an Offer

The best buyers become bankable before they start submitting offers.

This means cleaning up personal credit, saving for equity, preparing a net worth statement, and understanding what size of business your financial profile can support.

Prequalification conversations with lenders can save months of wasted time chasing deals that are not financeable.

When you walk into a negotiation already bankable, sellers take you more seriously and you can move faster.

Bankability Is a Strategy

Being bankable is not about luck. It is a strategy.

- Strong cash flow

- Clear repayment capacity

- Meaningful equity

- Relevant experience

- Clean credit

- Complete documentation

- Smart deal structure

- The right lender relationships

When these pieces are in place, financing becomes much easier.

Most deals that fail do not fail because the business is bad. They fail because the buyer was not prepared for the lending process.

If your goal is to buy a business using financing, start by building your bankable profile. Once you do, opportunities open up quickly and lenders start saying yes.

At the end of the day, lenders are betting on two things: the cash flow of the business and your ability to manage and repay the loan.

When those two pieces align, financing becomes much easier.

When they do not, even good businesses can struggle to secure funding.

If you want help preparing a bank ready acquisition file, structuring your deal, or understanding how much business you can afford, VI Business Brokers works with buyers across Canada to get them financeable and into the right business.

Becoming bankable is the first step to becoming an owner.