Need funding for your small business? Discover how the CSBFP lets the government guarantee 85% of loans to help you grow safely.

If you are buying or growing a business in Canada, you have probably come across the Canada Small Business Financing Program, often called CSBFP or CSBFL. It is one of the most useful tools available for small business financing, but it is also widely misunderstood.

Most people know the government guarantees up to 85% of the loan. What many do not realize is how strict the program is when it comes to what you can actually finance.

Let’s break it down in simple terms so you understand how it works and how it applies to real deals.

What is the Canada Small Business Financing Program

The Canada Small Business Financing Program is a federal initiative designed to help small businesses access loans through banks and credit unions.

The government does not lend money directly. Instead, it shares the risk with lenders by guaranteeing a large portion of the loan.

You can learn more directly from the official government page here:

https://ised-isde.canada.ca/site/canada-small-business-financing-program/en

This program exists to make it easier for businesses to get approved, especially when they do not have strong collateral or long operating history.

NOTE: One important thing to clarify is that the government is not actually lending you the money.

Instead, the loan comes from a bank or credit union, and the government simply guarantees a large portion of it. This means the lender is protected if something goes wrong, which is why they are often more willing to approve deals that might otherwise be declined.

How the 85% Government Guarantee Works

The biggest feature of the CSBFP is the government guarantee.

Here is how it works in simple terms:

- If a borrower defaults on a CSBFP loan, the Government of Canada will cover up to 85% of the lender’s eligible loss.

- This reduces the lender’s risk significantly and makes them more willing to approve deals they might otherwise decline.

Important to understand:

- You are still responsible for 100% of the loan

- The guarantee protects the lender, not the borrower

So while it improves your chances of getting financing, it does not reduce your obligation to repay.

What the CSBFP is Really Designed For

This is where most confusion happens.

The CSBFP is not a general business loan program. It is an asset based financing program.

That means it is specifically designed to finance identifiable business assets, not ownership of a corporation.

According to the official program guidelines, the loan must be tied to eligible assets and uses. It is not meant to fund equity transactions or ownership transfers through shares.

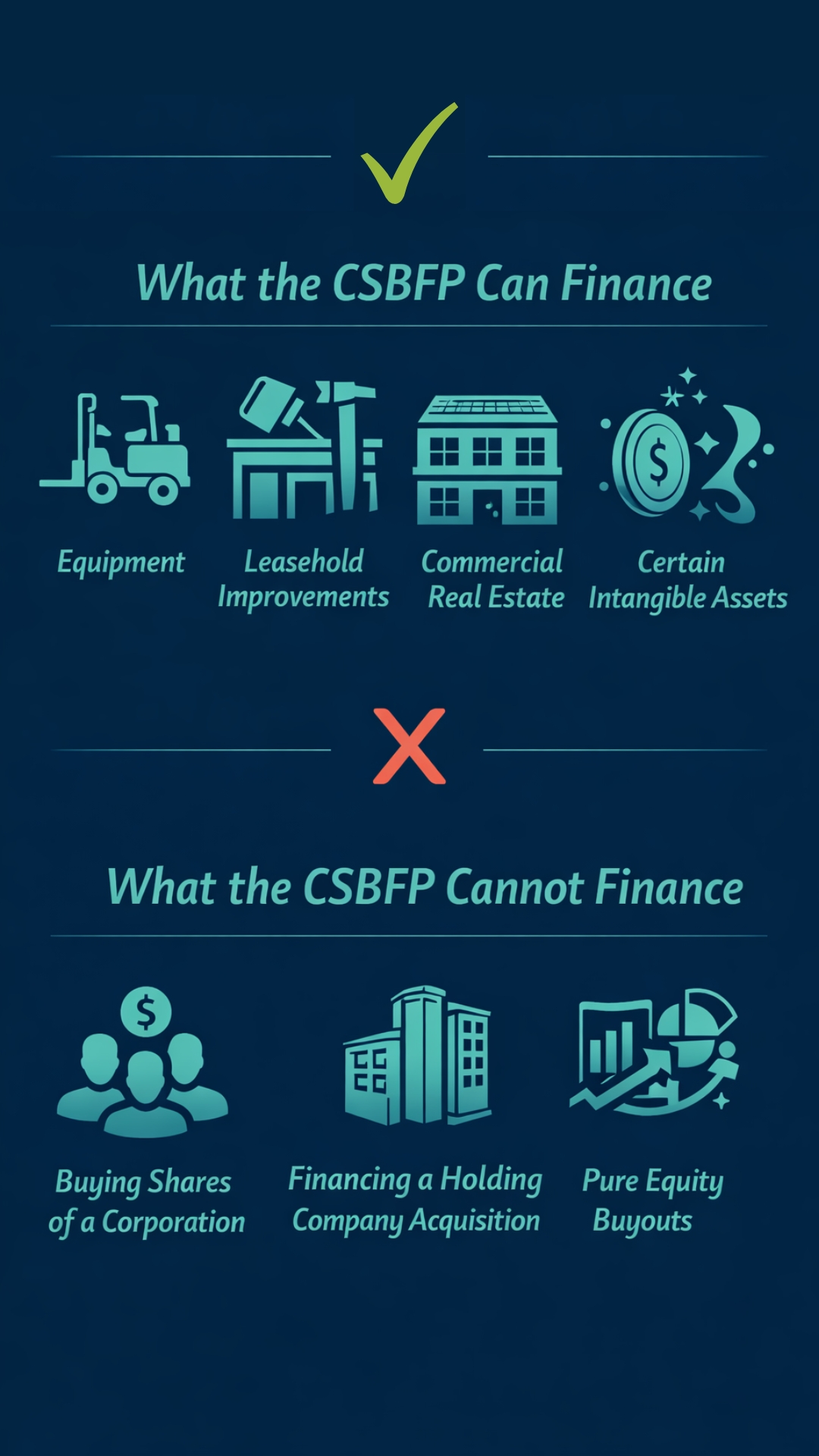

What the CSBFP Can Finance

Under the program, lenders can finance specific types of business assets.

These typically include:

- Equipment and machinery

- Leasehold improvements

- Commercial real estate

- Certain intangible assets tied to the business

In some cases, this also includes goodwill, but only when it is connected to an asset purchase structure.

A common example used by lenders is:

- Purchase of eligible assets of an existing business may qualify

- Other eligible business assets depending on lender approval

This is why the program is so powerful for buyers. It allows you to finance real, tangible parts of a business rather than relying entirely on personal capital, making it easier to acquire or grow a business with less money down.

What the CSBFP Cannot Finance

This is the most important part, especially if you are buying a business.

The CSBFP cannot be used for:

- Buying shares of a corporation

- Financing a holding company acquisition

- Pure equity buyouts

In simple terms:

- You cannot use CSBFP funds to purchase shares

In many cases, franchise purchases may also have restrictions depending on how the deal is structured and approved by the lender.

Why Deal Structure Matters More Than Anything

This is where things get very practical, especially in real transactions.

Whether you can use CSBFP or not often comes down to how the deal is structured.

Share Sale

If you are buying a business through a share purchase:

CSBFP → not usable

You will need other financing options such as:

- Traditional bank loans

- BDC financing

- Vendor take back financing

- Or a combination of all three

Asset Sale

If the deal is structured as an asset purchase:

CSBFP → usable

This is why many transactions are structured this way.

In an asset deal, the purchase price is allocated to specific items like:

- Equipment

- Leaseholds

- Furniture and fixtures

- Some goodwill depending on lender approval

This makes the deal much more “bankable” under CSBFP guidelines. For a deeper look at how buyers can improve their bankability in financing situations, see How to Be Bankable When Buying a Business in Canada, which explains the key factors lenders consider before approving acquisition financing.

How Brokers Structure Deals to Use CSBFP

In real transactions, this comes up all the time.

A business might initially be presented as a share sale, but once financing is considered, the structure often changes.

Typical approach:

- Convert share deal into asset purchase

Then break down the purchase price into:

- Tangible assets like equipment

- Leasehold improvements

- Eligible portions of goodwill

After that, financing is layered like this:

CSBFP loan for the asset portion

Vendor take back from the seller

Buyer equity injection

This combination is extremely common in small business acquisitions across Canada.

How Much You Can Borrow

Under the CSBFP, businesses can access:

Up to $1,000,000 for term loans

This can be used for a mix of:

- Equipment

- Property

- Improvements

- Eligible intangible assets

The exact structure depends on the lender and how the deal is put together.

In addition to term loans, some lenders may also offer:

Up to $150,000 for lines of credit

This can provide additional flexibility for working capital, although availability depends on the lender and deal structure.

Who is Eligible

To qualify for the program, your business must:

- Operate in Canada

- Be for profit

- Have annual revenues under 10 million dollars

Most small and medium sized businesses fall within this range, making the program widely accessible.

How to Apply

You do not apply through the government directly.

Instead, you apply through a participating lender such as a bank or credit union.

Basic steps:

- Prepare your business plan and financials

- Present the deal and asset breakdown

- Apply through a lender offering CSBFP

- Get approval based on lender criteria

The lender then registers the loan under the program.

Pros and Cons of the CSBFP

Pros

- Higher approval chances due to government guarantee

- Access to larger loan amounts

- Great for asset heavy business purchases

Cons

- Cannot be used for share purchases

- Still requires strong application and structure

- Limited flexibility compared to traditional loans

- Not all lenders offer the same flexibility, and approval still depends heavily on the strength of the borrower and the deal

Where to Learn More

If you want the official overview of the program or want to confirm details, check out the Government of Canada’s guidelines on the CSBFP and how it works with lenders and businesses:

The Canada Small Business Financing Program (CSBFP) is not a magic loan, but it is a powerful tool for small business owners who want to grow without putting everything on the line upfront. By having the government guarantee up to 85 % of the loan, lenders are more willing to take chances on small businesses but borrowers are still responsible for repaying the full amount.

Whether you’re buying equipment, renovating space, or expanding your operations, CSBFP could be the financing boost you need to take your business to the next level.

If you’re considering a loan under this program, it’s wise to talk directly with your bank or a financial advisor who understands how to structure CSBFP financing for your specific needs.