Applying for a commercial loan in Canada can feel overwhelming, especially if you are buying a business or expanding for the first time. The good news is that lenders follow a fairly predictable process. Once you understand the steps and prepare properly, getting approved becomes much easier.

This guide walks you through the Canadian commercial loan process in plain language so you know what to expect and how to improve your chances of success.

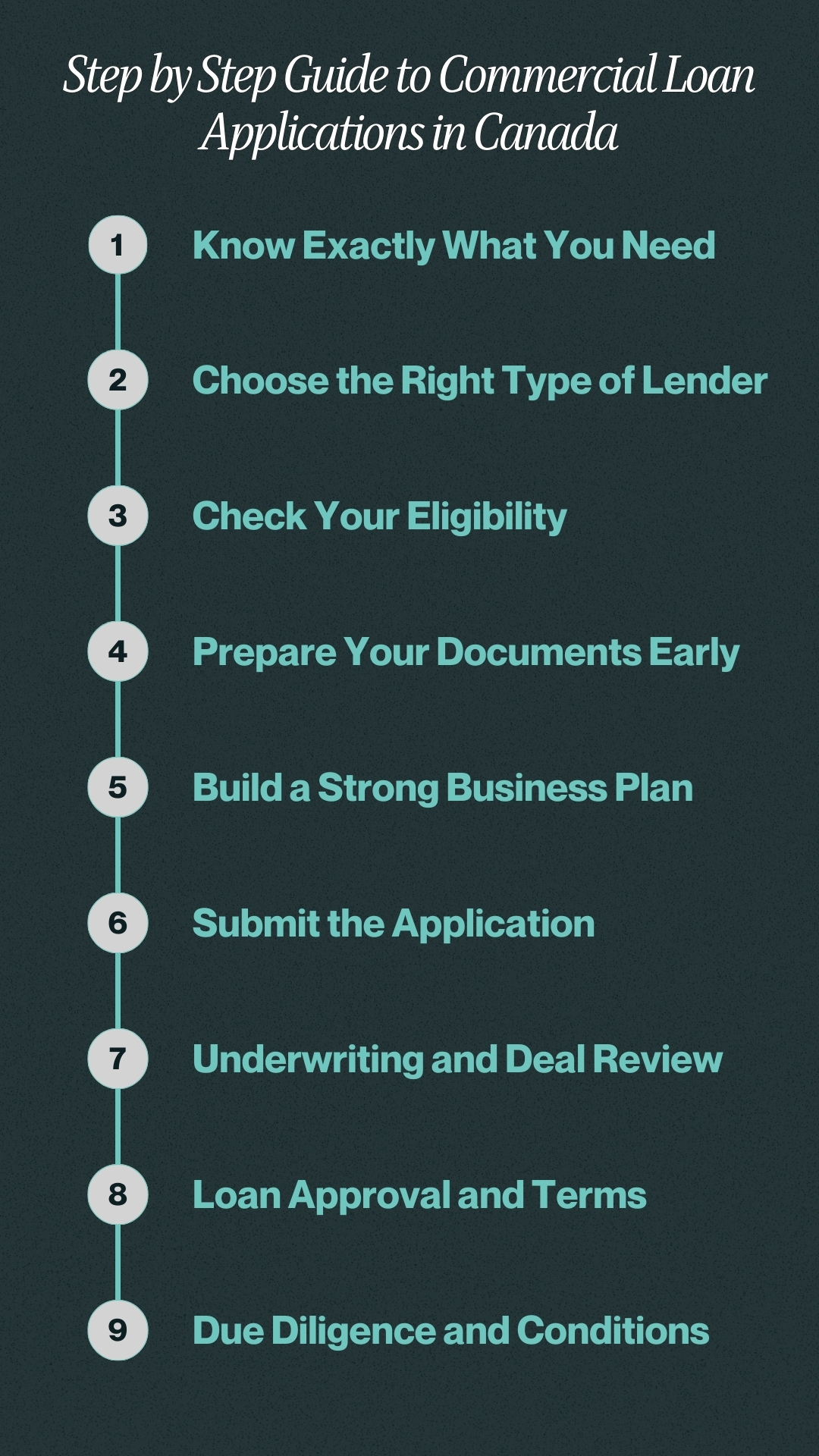

Step 1: Know Exactly What You Need

Before talking to any lender, you need to be clear on three things. How much money you need. What the funds will be used for. How the loan will be repaid.

Lenders care less about the idea and more about the numbers. They want to see that the loan has a clear purpose such as buying a business, purchasing equipment, funding leasehold improvements, or covering working capital. They also want to know that the cash flow from the business can comfortably cover the loan payments.

If you are buying a business, be ready to explain the purchase price, down payment, and expected income after the acquisition.

Step 2: Choose the Right Type of Lender

In Canada you generally have four main commercial lending options. Traditional banks and credit unions. The Business Development Bank of Canada. Government backed programs like the Canada Small Business Financing Program. Alternative lenders.

Each lender has a different risk tolerance. Banks usually offer the best rates but require strong financials and collateral. BDC is more flexible and focuses on business growth. Government backed programs help when you have a solid deal but not enough collateral.

Choosing the right lender early saves time and prevents unnecessary declines.

Step 3: Check Your Eligibility

Most Canadian lenders look at similar baseline criteria. Your business should be registered in Canada and operating for at least twelve to twenty four months with revenue. Good personal credit also helps.

Lenders will also evaluate profitability, industry risk, and your experience managing a business. Even if you are buying a company, they want to see that you have relevant skills or a strong management team in place.

If you do not meet bank requirements, BDC or a government guaranteed loan may still be an option.

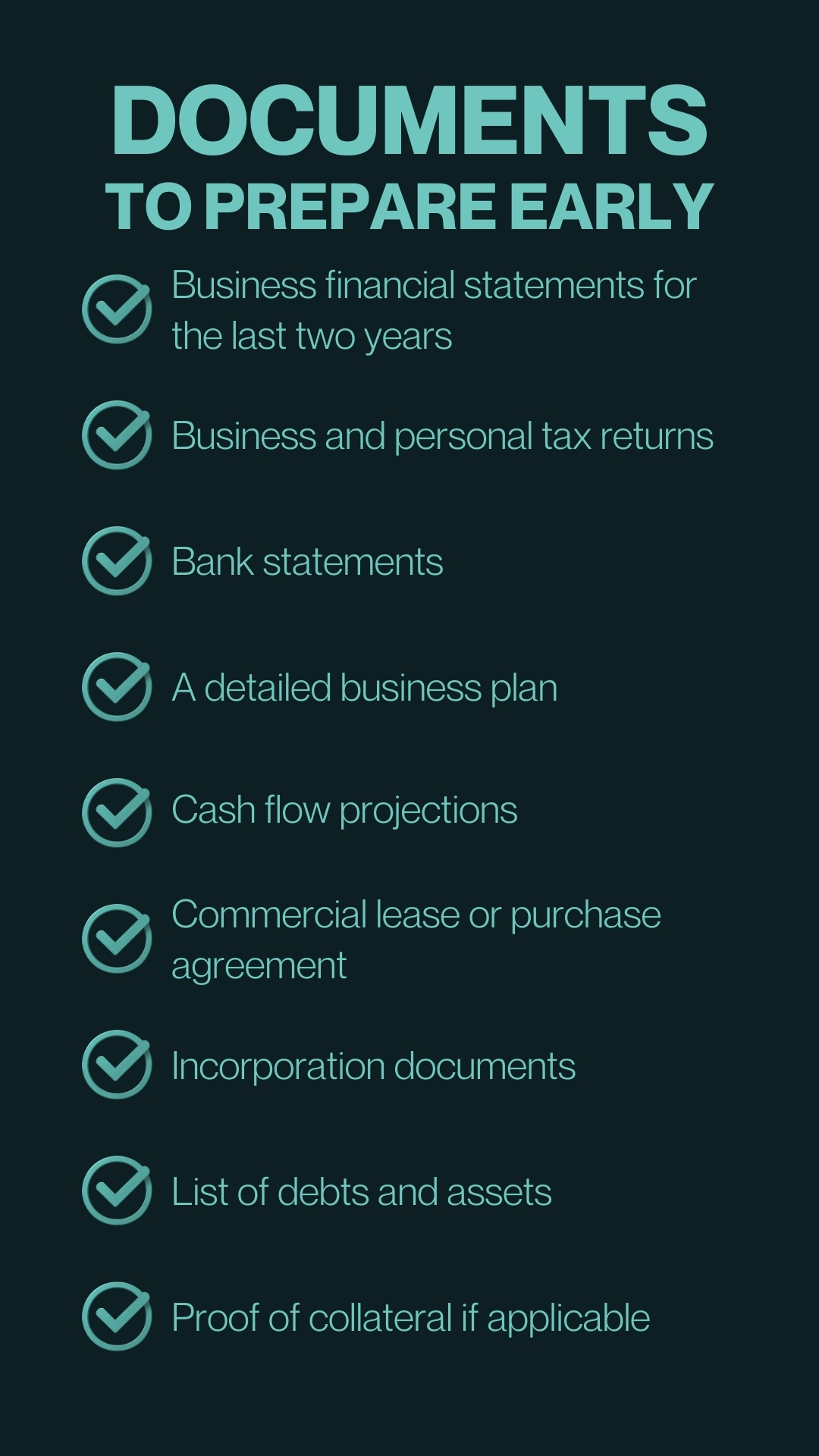

Step 4: Prepare Your Documents Early

This is where most applications succeed or fail. Having a complete document package speeds up approval and makes you look professional.

Typical Canadian commercial loan documents include

- Business financial statements for the last two years

- Business and personal tax returns

- Bank statements

- A detailed business plan

- Cash flow projections

- Commercial lease or purchase agreement

- Incorporation documents

- List of debts and assets

- Proof of collateral if applicable

BDC may also request a void cheque, shareholder information, and government issued ID.

For commercial real estate or larger deals, lenders can ask for appraisals, environmental reports, and lease summaries.

Preparing these in advance can cut weeks off the process.

Step 5: Build a Strong Business Plan

Your business plan does not need to be long but it must answer key lender questions. What does the business do. Who are the customers. What is the competitive advantage. How will the loan increase revenue or efficiency.

Most importantly, include realistic financial projections. Lenders want to see monthly cash flow forecasts that show you can handle debt payments while still operating comfortably.

If you are buying a business, include historical financials from the seller and your plan for growth after takeover.

Improve Your Bankability Before Applying

Before submitting your loan application, it’s important to understand what makes a buyer bankable in the eyes of lenders especially when acquiring a business. A strong cash flow, solid equity contribution, credible management experience, and professional documentation can significantly increase your chances of approval.

For a detailed guide on how to strengthen these aspects before applying, see How to Be Bankable When Buying a Business in Canada.

This additional resource covers key lender expectations and strategies to enhance your financing prospects.

Step 6: Submit the Application

Once your documents are ready, you complete the formal loan application. This can be done online or through a commercial banker.

You will provide basic details such as business information, ownership structure, loan amount, and intended use of funds. Some lenders will also run credit checks on all owners and guarantors.

After submission, a lender or advisor will contact you to review the deal and request any missing documents.

Step 7: Underwriting and Deal Review

This is the stage where the lender analyzes your application in detail. They review financial ratios, debt service coverage, credit history, and collateral. They also assess the risk of the industry and the strength of the management team.

If you are buying a business, they will evaluate whether the cash flow supports the loan and whether the purchase price is reasonable.

This stage can take a few days for small loans or several weeks for larger and more complex transactions. Providing documents quickly helps move things along.

Step 8: Loan Approval and Terms

If approved, the lender issues a loan offer outlining the amount, interest rate, amortization, repayment schedule, and any conditions.

Interest rates in Canada are usually based on a base rate plus a risk premium that depends on your credit and financial strength.

You may also see requirements such as personal guarantees, collateral, insurance, or financial reporting covenants.

Review these terms carefully before signing.

Step 9: Due Diligence and Conditions

Most commercial loan approvals come with conditions that must be satisfied before funding. These can include

- Updated financial statements

- Proof of down payment

- Signed purchase agreements

- Appraisals or environmental reports

- Corporate legal documents

Meeting these conditions is often called clearing conditions. Once completed, the loan moves to funding.

Step 10: Funding and Closing

After all documents are signed and conditions met, the lender releases the funds. For business acquisitions, the money usually flows through lawyers and closes on the same day as the purchase.

At this point you begin making regular loan payments based on the agreed schedule.

Common Reasons Commercial Loans Get Declined

Understanding why loans fail can help you avoid mistakes. The most common issues include

- Incomplete document packages

- Unrealistic financial projections

- Weak cash flow

- Poor personal credit

- Lack of industry experience

- Overpaying for a business

Many of these problems can be fixed before applying if you work with an experienced advisor.

Tips to Improve Your Approval Chances

Securing a commercial loan in Canada is easier when you approach the process strategically. Lenders are looking for borrowers who are organized, responsible, and financially prepared. By taking steps ahead of time to strengthen your financial profile and presenting a clear, professional application, you increase your likelihood of approval and may even get better terms. Small improvements in preparation can make a big difference in how a lender views your application.

Here are some practical steps you can take to improve your chances:

-

Start preparing early: Begin gathering documents, reviewing your finances, and researching lenders at least two to three months before you need funding. Early preparation helps you avoid last-minute surprises.

-

Keep personal and business credit clean: Lenders pay close attention to credit history. Pay down debts, avoid late payments, and resolve any issues that could appear on a credit report.

-

Maintain accurate financial statements: Up-to-date and organized financial statements make your business look professional and trustworthy. This includes balance sheets, income statements, and cash flow reports.

-

Show a clear down payment and liquidity: Demonstrating that you have sufficient personal or business funds available shows lenders that you can handle the investment and unexpected expenses.

-

Choose the right lender for your deal: Not all lenders are the same. Some prefer stable businesses, while others are open to riskier ventures. Match your business type and financial situation to the right lender.

-

Present a simple and logical business plan: Lenders want clarity, not complexity. Clearly explain your business model, revenue projections, and how the loan will help the business grow. A straightforward plan makes you appear organized and confident.

A well-prepared application signals to lenders that you are low risk and serious about the loan. By taking the time to strengthen your financial profile and present your plan clearly, you set yourself apart from other applicants and make the approval process smoother and faster.

Securing a Commercial Loan

Getting a commercial loan in Canada is not about luck. It is about preparation, clarity, and choosing the right financing partner.

When you understand the process and present a strong financial story, lenders are far more likely to say yes. Whether you are buying a business, expanding operations, or investing in commercial real estate, following a step by step approach makes the journey smoother and faster.

If you are planning to acquire a business and need guidance on financing, working with professionals who understand both deal structure and lender requirements can significantly increase your chances of approval.