")

If you are buying a business, one of the first financial terms you will encounter is EBITDA. Soon after, you may also hear terms like Adjusted EBITDA and Seller’s Discretionary Earnings, commonly called SDE.

These terms are closely related, but they are not exactly the same.

Many buyers mistakenly assume that Adjusted EBITDA and SDE are interchangeable. While they both aim to show the true earning power of a business, they are generally used for different sizes and types of companies.

Understanding the difference between EBITDA, Adjusted EBITDA, and SDE is important because these numbers directly affect:

- Business valuation

- Financing approvals

- Buyer cash flow expectations

- Negotiation strategy

- Risk assessment

For small business buyers especially, misunderstanding these metrics can lead to overpaying for a business or misunderstanding how much income the company can realistically generate after takeover.

What is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization.

It is a financial metric used to measure the operating profitability of a business before financing decisions, tax structures, and certain accounting adjustments.

The formula looks like this:

Net Income

- Interest

- Taxes

- Depreciation

- Amortization

= EBITDA

EBITDA is commonly used because it removes variables that may differ from one company to another, including:

- Loan structures

- Tax situations

- Accounting methods

- Depreciation schedules

This makes it easier for investors and buyers to compare businesses objectively.

Larger corporations, institutional investors, and private equity groups often rely heavily on EBITDA because ownership is usually separate from daily operations.

In these businesses, the owner may not personally generate revenue or manage day to day activities.

Why EBITDA Works for Larger Businesses

EBITDA is most useful when a company already has:

- A management team

- Multiple employees handling operations

- Professional accounting systems

- Separate ownership and management

- Several shareholders or investors

In these situations, executive salaries are treated as normal operating expenses.

For example, if a manufacturing company employs a CEO earning $250,000 annually, that compensation remains part of operating expenses because the company would still need someone in that role after acquisition.

This is why EBITDA is commonly used in larger acquisitions and corporate transactions.

The Problem with EBITDA in Small Businesses

Most small businesses do not operate like corporations.

Small business owners often:

- Manage employees

- Handle customer relationships

- Perform sales

- Run daily operations

- Work directly in service delivery

- Run some personal expenses through the business

In these businesses, owner compensation is often part of the economic benefit of ownership rather than a traditional operating expense.

That creates a problem with EBITDA.

If you only looked at EBITDA for an owner operated company, you could significantly underestimate the financial benefit available to a buyer.

This is why small business brokers and buyers often rely more heavily on Adjusted EBITDA or SDE.

What is Adjusted EBITDA?

Adjusted EBITDA starts with standard EBITDA and then adds back unusual, non recurring, or discretionary expenses to show the normalized earning power of the business.

Typical adjustments may include:

- One time legal fees

- Non recurring repairs

- Owner personal expenses

- Excessive travel or entertainment

- Family members on payroll not active in the business

- Above market owner compensation

The goal is to show what the business would realistically earn under normal operations.

Adjusted EBITDA is commonly used for medium sized businesses and lower middle market companies where ownership may still influence expenses but professional management structures also exist.

What is SDE?

Seller’s Discretionary Earnings, or SDE, is similar to Adjusted EBITDA but goes one step further.

SDE includes all the adjustments found in Adjusted EBITDA, but it also adds back the owner’s full compensation, benefits, and personal perks.

The formula typically looks like this:

Net Profit

- Interest

- Taxes

- Depreciation

- Amortization

- Owner Compensation

- Non Recurring Expenses

- Personal or Discretionary Expenses

= Seller’s Discretionary Earnings

SDE answers an important question for buyers:

“If I bought this business and personally operated it full time, how much total financial benefit could I receive?”

That is why SDE is most commonly used for:

- Small businesses

- Main street businesses

- Owner operated companies

- Family businesses

- First time buyer acquisitions

Examples include:

- Restaurants

- Retail stores

- Small trades businesses

- Local service companies

- Independent professional practices

Are Adjusted EBITDA and SDE the Same?

Not exactly.

They are very similar because both metrics attempt to normalize earnings and remove unusual expenses. However, the biggest difference is owner compensation.

Similarities Between Adjusted EBITDA and SDE

Both metrics:

- Remove one time expenses

- Add back discretionary spending

- Normalize financial statements

- Help buyers understand true cash flow

- Are commonly used in business valuations

Main Difference Between Adjusted EBITDA and SDE

The largest difference is how owner compensation is treated.

Adjusted EBITDA:

- Usually assumes management remains in place

- May normalize owner salary to market rates

- Is commonly used for medium sized businesses

SDE:

- Adds back the owner’s entire compensation package

- Assumes the buyer will actively operate the business

- Is commonly used for smaller owner operated companies

In simple terms:

- Adjusted EBITDA measures business cash flow

- SDE measures owner benefit

Main Differences Between EBITDA, Adjusted EBITDA, and SDE

EBITDA

- Measures operational profitability

- Does not adjust for unusual owner expenses

- Owner salary stays as an expense

- Commonly used for larger businesses

Adjusted EBITDA

- Starts with EBITDA

- Removes unusual or non recurring expenses

- May adjust excessive owner compensation

- Commonly used for mid sized companies

SDE

- Includes all Adjusted EBITDA add backs

- Adds back full owner compensation and perks

- Measures total financial benefit to an owner operator

- Commonly used for small businesses

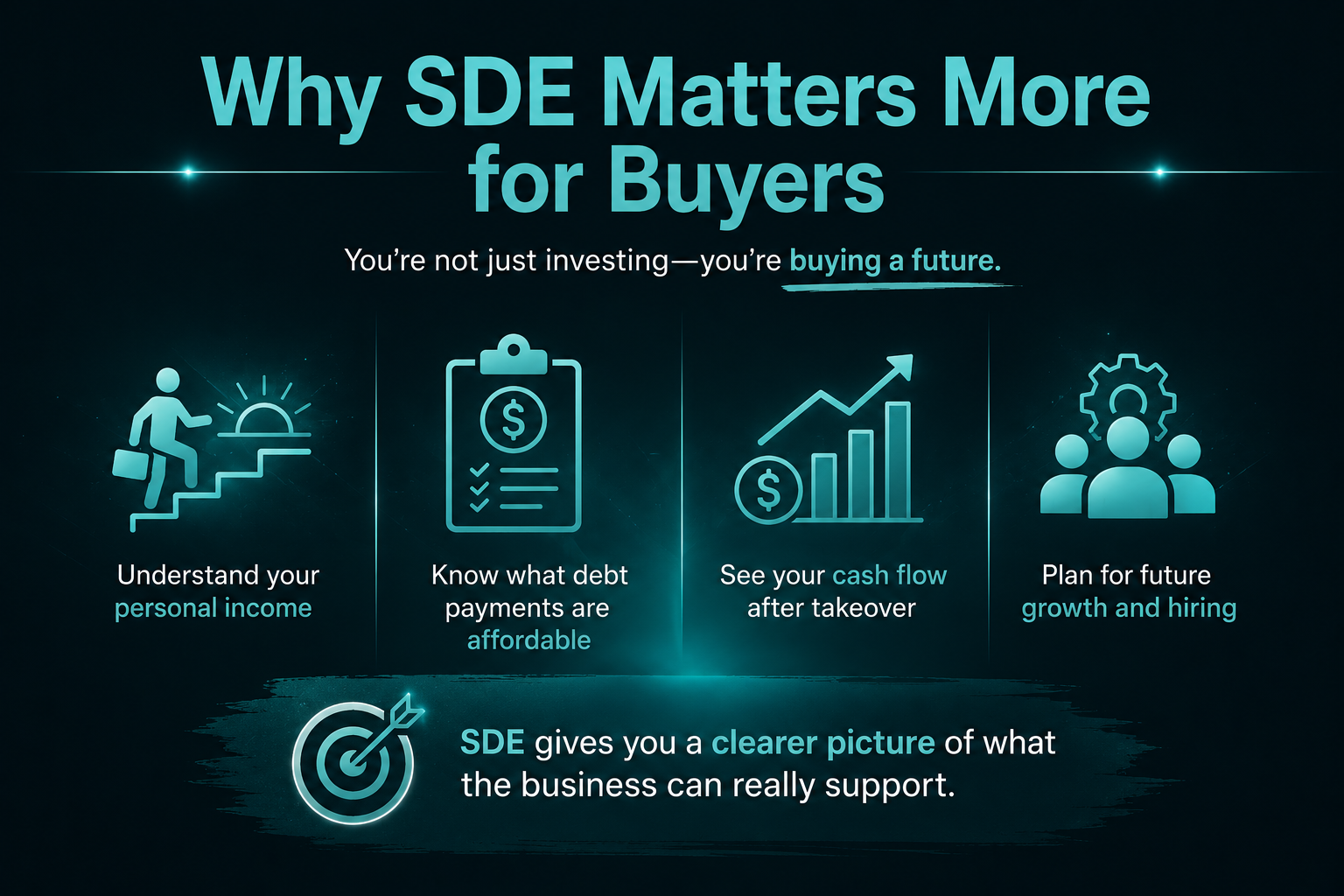

Why SDE Matters More for Buyers

For most small business acquisitions, buyers are not passive investors.

They are buying themselves a job, income stream, and future growth opportunity.

That means buyers need to understand:

- How much money they can personally earn

- Whether debt payments are affordable

- What cash flow will look like after takeover

- Whether the business can support future hiring

SDE provides a clearer picture of these realities than EBITDA does.

This is especially important in Canada’s small business market, where many businesses are still heavily owner dependent.

The Business Development Bank of Canada regularly discuss the importance of cash flow analysis and operational earnings when evaluating businesses for financing and growth.

EBITDA vs SDE: Simple Example

Let’s look at a simplified example.

A small plumbing company reports:

• Net Profit: $80,000

• Owner Salary: $100,000

• Interest: $10,000

• Depreciation: $15,000

• Personal Vehicle Expense: $12,000

EBITDA Calculation

$80,000 Net Profit

- $10,000 Interest

- $15,000 Depreciation

= $105,000 EBITDA

Adjusted EBITDA

$105,000 EBITDA

+ $12,000 Personal Vehicle Expense

= $117,000 Adjusted EBITDA

SDE Calculation

$117,000 Adjusted EBITDA

+ $100,000 Owner Salary

= $217,000 SDE

That is a major difference.

If a buyer only focused on EBITDA, they may believe the business generates roughly $100,000 annually. But a working owner could potentially receive over $200,000 in total financial benefit.

Which Metric Should Buyers Use?

The answer depends on the type of business being acquired.

Generally speaking:

EBITDA is more useful for:

• Larger companies

• Businesses with management teams

• Semi absentee ownership models

• Corporate acquisitions

• Private equity transactions

Adjusted EBITDA is more useful for:

- Lower middle market businesses

- Companies transitioning toward professional management

- Businesses with some discretionary owner expenses

SDE is more useful for:

• Small businesses

• Owner operated companies

• Main street businesses

• Family businesses

• First time buyers

In many transactions under a few million dollars, SDE is usually the more relevant number.

This is especially true for owner operated companies, where cash flow often matters more than overall revenue. Buyers researching market pricing may also want to understand what the average business valuation looks like across different industries and business sizes.

Why Accurate Financial Analysis Matters

One of the biggest mistakes buyers make is focusing only on revenue.

Revenue alone does not determine profitability.

A company generating millions in annual sales may still produce very little owner income if operating costs are too high.

That is why experienced buyers, lenders, accountants, and brokers focus heavily on EBITDA, Adjusted EBITDA, and SDE during due diligence.

These metrics help buyers understand:

- True earning power

- Debt service capability

- Future hiring potential

- Operational efficiency

- Realistic owner income

That is why experienced buyers, lenders, and brokers spend far more time analyzing cash flow metrics like SDE and EBITDA. Understanding these metrics is also an important part of learning how to value a business properly before making an acquisition.

The Canadian Federation of Independent Business also emphasizes the importance of understanding profitability and operating costs when evaluating small business performance.

Understanding Which Metric Matters Most

Understanding the difference between EBITDA, Adjusted EBITDA, and SDE is essential when buying a business.

EBITDA works best for larger companies where ownership and operations are separate.

Adjusted EBITDA helps normalize earnings by removing unusual or discretionary expenses.

SDE goes one step further by measuring the total financial benefit available to an owner operator.

For most small business acquisitions, SDE often provides the clearest picture of what a buyer can realistically earn after takeover.

Learning how to properly analyze these metrics can help buyers avoid costly mistakes, negotiate better deals, and make smarter acquisition decisions.